Tax Lien Investing Explained: A Complete Guide for Real Estate Pros

When most people think of tax lien investing, they may think it’s one of those rarely discussed real estate niches that sounds complicated, risky, or reserved only for those who specialize in the field. In all reality, it’s one of the oldest, most misunderstood, and often most overlooked opportunities in real estate’s multi-faceted industry. Many agents, brokers, investors, and even appraisers hear about tax liens in passing but never take the time to understand how they actually work, or how they can fit into a broader real estate business.

Our guide breaks down tax lien investing in plain language. No hype, no gimmicks. Just a clear explanation of what tax liens are, how the process works, where real estate professionals can fit in, and why this strategy continues to attract investors looking for alternative paths to returns and inventory. If you’ve ever wanted a practical, real-world explanation of tax lien investing, this is it.

What Is a Tax Lien, Really?

A tax lien is created when a property owner fails to pay their property taxes. Local governments still need revenue to fund schools, roads, and public services, so instead of waiting indefinitely for payment, they place a lien on the property for the unpaid taxes, plus interest and penalties. That lien represents a legal claim against the property. In many states, counties then sell that lien to investors. The investor pays the delinquent taxes upfront, and in exchange, earns the right to collect the debt plus interest when the owner eventually pays.

In simple terms, the investor is stepping in to cover the owner’s tax bill and gets compensated for doing so.

Tax Lien Investing vs Tax Deed Investing

One of the most significant sources of confusion in this space is the difference between tax lien states and tax deed states.

In tax lien states, investors buy the lien itself, not the property. The property owner usually has a redemption period, often ranging from six months to several years, during which they can repay the taxes plus interest. If they do, the investor gets paid, and the lien is released. In tax deed states, the county eventually sells the property itself (often to the highest bidder) if taxes remain unpaid. The investor may end up owning the property outright.

Our article focuses primarily on tax lien investing, where the goal is typically earning interest, not taking ownership of the property, although that can happen in rare cases.

Why Tax Lien Investing Exists at All

From a government standpoint, tax lien sales often solve a local cash flow problem. Counties cannot operate on unpaid promises (like unpaid taxes on real estate within said county). Selling liens allows them to recover funds immediately without managing collections themselves.

From an investor standpoint, tax liens offer something that traditional real estate often doesn’t: predictable, statutory returns. Interest rates are set by law, not market speculation. And in some states, returns can even range from mid single digits to well into the double digits (10’s of thousands of dollars).

For real estate professionals who are already comfortable with property data, public records, and due diligence, tax liens are a natural extension of the skills they already use every day.

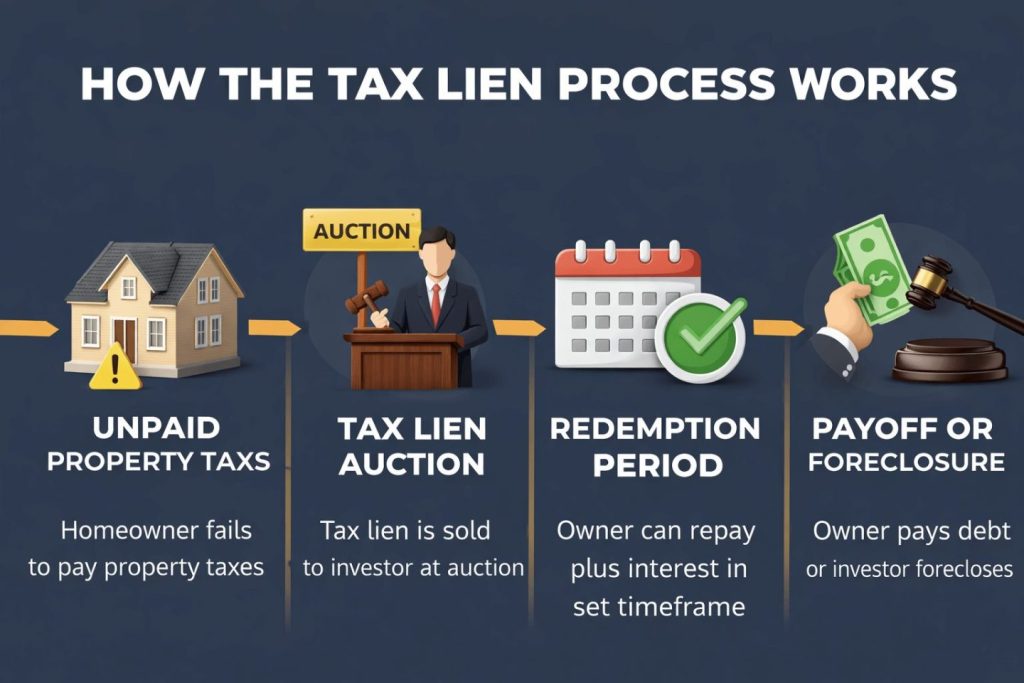

How the Tax Lien Process Works Step by Step

While details vary by state and county, the general process is pretty consistent.

First, the property owner falls behind on taxes. After a certain period, the county records a tax lien against the property. Next, the county schedules a tax lien sale or auction. These can be held in person or online, depending on the jurisdiction. Investors register for the auction and bid on liens. In many states, bidding is based on the interest rate the investor is willing to accept, not the price of the lien itself. Once the lien is purchased, the investor waits through the redemption period. If the owner pays the taxes, the investor receives the original amount paid plus interest. If the owner does not redeem within the allowed timeframe, the investor may have the right to initiate foreclosure proceedings, depending on that state’s law.

The Role of Interest Rates and Penalties

One of the main reasons investors are drawn to tax liens is the interest structure. These rates are not negotiated. They are defined by statute.

Some states use simple interest, others use penalty-based systems, and some use a hybrid approach. In certain jurisdictions, even a short redemption period can result in a strong annualized return. For real estate professionals used to commission-based income or long-hold strategies, tax liens can feel refreshingly straightforward. The math is clear, the rules are defined, and timelines are established upfront.

Due Diligence Matters More Than Most People Realize

One of the biggest mistakes new tax lien investors make is assuming that all liens are safe simply because they are backed by real estate. That assumption can be costly. Not all properties are equal. Some liens are attached to landlocked parcels, environmentally contaminated lots, or properties already burdened by superior liens.

Smart investors research properties before bidding. They review location, assessed value, zoning, access, and any existing encumbrances. Just because taxes are owed does not mean the property itself is desirable or even usable. This is where real estate professionals have a major advantage. Understanding property data, market value, and land use gives you a leg up over investors who are simply chasing yield.

What Happens If You End Up With the Property?

Although most tax liens redeem the investor purchasing the lien, occasionally they do not. In those cases, the investor may have the right to foreclose and potentially take ownership. This outcome should never be treated casually. Foreclosure involves legal costs, timelines, and compliance with state-specific procedures.

For agents and brokers, however, this scenario can turn into an opportunity. Acquiring property through a tax lien foreclosure can create inventory where none previously existed. It can also lead to listings, resale opportunities, or long-term holds. The key is understanding that the exit strategy must be considered before the lien is ever purchased.

How Real Estate Professionals Can Use Tax Liens Strategically

Tax lien investing does not have to be an all-or-nothing strategy. Many professionals use it as a complement to their existing business. Agents may invest personally to diversify income streams that are not tied directly to transactions. Brokers may use tax lien data to identify distressed property owners who could benefit from guidance before issues escalate. Appraisers and land specialists often use tax delinquency trends to understand emerging risk or opportunity areas within a market. Even if you never buy a lien, understanding how tax liens work can make you more valuable to clients navigating distressed situations.

Common Myths About Tax Lien Investing

One of the most persistent myths is that tax lien investors are taking advantage of struggling homeowners. In reality, tax lien investing is a structured, legal process designed to keep municipalities funded while giving owners a clear path to redemption. Another myth is that investors regularly acquire properties for pennies on the dollar. While that can happen, it is far from the norm. Most liens redeem, and most investors earn interest, not property. There is also a misconception that tax lien investing is passive. It is not. While it may be less hands-on than rentals, it still requires research, tracking deadlines, and understanding legal procedures.

Risks You Should Actually Take Seriously

Like any investment strategy, tax liens come with real risks. Legislative changes can alter interest rates or redemption rules. Poor property research can leave investors holding liens tied to undesirable assets. Liquidity is another factor. Funds are often tied up until redemption or foreclosure. This is not a short-term flip strategy in most cases. For professionals used to controlling timelines through listings and closings, this lack of immediate control can feel uncomfortable. That does not make it bad, but it does make it different.

Why Tax Lien Knowledge Is Becoming More Relevant

As property taxes rise in many areas, delinquency rates often follow. Economic shifts, insurance costs, and changing affordability dynamics all contribute. That means tax liens are not going away. If anything, they are becoming a more visible part of the real estate ecosystem. Professionals who understand this space are better equipped to advise clients, identify early warning signs, and create alternative income strategies that are not dependent on market cycles alone.

Final Thoughts

Tax lien investing is not a shortcut, a secret loophole, or a guaranteed windfall. It is a structured, rules-based strategy that rewards patience, research, and local market knowledge. For real estate professionals, it offers more than just potential returns. It offers insight into distressed properties, local tax dynamics, and opportunities that most of the industry ignores. Whether you choose to invest directly or simply understand the process, tax liens are one more tool in the toolbox. And in a market that continues to evolve, having more tools, not fewer, is what separates adaptable professionals from those who get left behind.

If you want to stay ahead in real estate, understanding tax liens is no longer optional. It is part of the bigger picture.